Global PC sales rise: Here’s the leader

The global PC market experienced a significant recovery in the second quarter of 2025. According to data shared by market research firm Canalys, desktop and laptop shipments increased by 7.4% year-over-year, reaching 67.6 million units. This increase marked the largest annual growth in the post-pandemic period. However, industry experts are cautious about the longevity of this growth.

Global PC sales are on the rise

Multiple factors are driving this increase. First and foremost, the upcoming end of support for Windows 10 in October 2025 has prompted many companies to update their PC fleets. Enterprise users have shown a tendency to migrate to Windows 11-compatible systems before support ends. This has led to a significant increase in manufacturers’ corporate shipments.

Furthermore, the growing interest in AI-enabled computer systems has led to demand for new hardware. Furthermore, manufacturers have accelerated their shipments in response to the possibility of tariffs revived by the Trump administration in the US, providing short-term market activity.

On the consumer side, the picture is more balanced. While the widespread adoption of Windows 11 has led individual users to upgrade their systems, growth has been more limited compared to previous quarters. Analysts note that high prices and product saturation in the consumer segment are contributing factors.

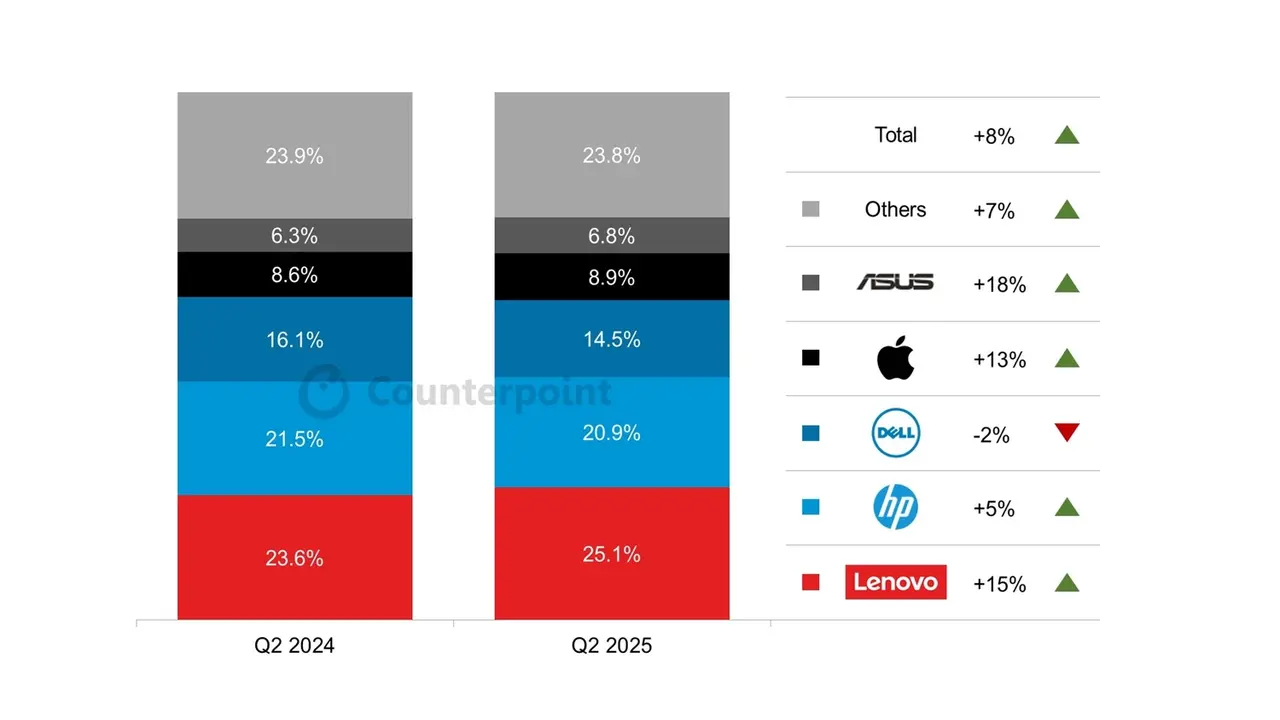

Brand-by-brand, Lenovo maintains its leadership with 25% market share and 15% annual growth. HP came in second with 20.9%. Dell remains in third place with 14.5%, but experienced a slight market share loss this quarter.

Apple saw 13% growth, driven by the new M4-powered MacBooks. The company’s total market share stood at 8.9%. Asus was the fastest-growing brand, reaching 6.8% market share and achieving 18% growth during the quarter.

Analysts predict that the sector will remain vibrant in the short term, but trade tensions, customs policies, and supply chain uncertainties have the potential to impact the overall outlook. Political tensions, particularly between China and the US, are expected to put pressure on production and distribution processes.

Your comment has been submitted,

it will be published after approval.